Introduction:

The term debasement is largely a subject of context, and that context has changed significantly over the last 500 years. Coins that once circulated as the exclusive means of payment are seldom used today, with payment becoming increasingly digital. Prior to the world of Paypal, Venmo, Bitcoin, and FDIC guarantees, people worried about money’s tangible value. Before we discuss modern debasement in the form of currency devaluation, we will recap the Locke and Lowndes debate mentioned prior.

Historical debates:

During the late 17thcentury there were three chief problems (among others) facing England and the British Pound: counterfeiting of coin, war, and the corresponding liquidity crisis. This myriad of problems led to a sequence of trial and error events, but come 1694, the debate was clear: should England debase its currency or not?

Locke & the anti-debasement position

John Locke’s position was to not debase British coin (not to alter the weight or fineness of silver in the coins). Locke claimed debased coin would be detrimental to both the king and businesses. Both parties would receive less money when repaid by their debtors than expected if debasement was to become a reality.[1]To maintain the durability of coins, Locke advocated mixing silver with metals like copper to form an alloy – but in the process stressed keeping the sterling standard unchanged (the amount of silver in each coin). He believed coins held only as much value as the metal they were composed of, thereby disregarding a coin’s face value entirely. This intrinsic value was the sole factor in determining what coins were actually worth.[2]For this reason, reducing the amount of metal in coins was detrimental to all stakeholders. Since the power of money was rooted in the physical amount of silver each coin possessed, altering that amount, he believed, would lead to inflation. Further, in accord with his argument, he wrote that clipped coin should only pass for its value by weight. If the crown elected to proceed with debasing the pound, Locke theorized trade would slow, because a debased currency is not as well received by counterparties who expect more by means of weight.[3]

Lowndes & the pro-debasement position

William Lowndes supported the opposite position by encouraging debasement. In altering the weight of coins (not fineness), more coins could be produced in an environment where there was alre

ady a severe paucity of silver. This would also ameliorate the silver melting problem. At the time, the value of bullion, or un-minted silver, was worth more than its value as coin. Because people received more money for silver when melted, that’s exactly what they did despite its illegality. Debasing would incentivize minting by giving people a greater value in coin for their silver than their silver would otherwise be worth as bullion.[4]If successful, this effort would help create a favorable balance of trade and stop silver from being sent overseas where it fetched a price premium relative to its value in England.[5]Old and clipped coins circulated at face value in England, while all the newly minted and heavier coins were either kept and melted or sent overseas, drastically offsetting the balance of trade.

England eventually heeded Locke’s advice and reinstalled confidence in a nervous public by avoiding debasement. The result saved the bank of England and its notes which circulated at a heavy discount.

Contemporary view points and applications:

Viewing debasement through a modern lens tells a different story. Debasement almost always refers to metallic currencies, which are largely out of circulation today. Even cash has dwindled in its importance – estimates predict cash will only make up 11.7% of US GDP by 2020.[6]For these reasons, we will focus on debates regarding the effectiveness of devaluation in place of debasement.

Debasement’s sibling – devaluation

Devaluation, much like debasement, is the deliberate devaluation of a currency relative to another country or general standard.[7]The primary reason countries consider devaluation attractive is because it promotes a favorable balance of trade. This is the exact position Lowndes was articulating in 1695. A cheaper, devalued currency, fuels exports as buyers pay less for goods produced in their own currency. However, higher domestic demand also serves as a catalyst for in

flation which is often considered a side effect of devaluation. Inflation is simply a steady rise in prices of goods, usually measured using the Consumer Price Index (CPI). Locke feared debasement because he saw inflation as

its byproduct. The two dominant causes of the phenomena are demand-pull (over expansion of the money supply leading to a reduction in currency valuation) and cost-push (supply shortages and strong demand causing increased prices).[8]

Modern devaluation – challenging traditional theories

The same economic principles that governed debasement in England centuries ago translate well to devaluation. Brazils finance minister coined the phrase “currency war” when he complained about the relatively cheap Chinese Yuan, which he claimed provided China with an unjust trade benefit.[9]The theory remains unchanged: cheaper currencies make foreign goods more expensive and encourage domestic production at a lower price. But, the model breaks down in a politically charged marketplace, namely in the form of a retaliatory devaluation. This sequence of events triggers a currency war, which defuses devaluation’s initial benefits.

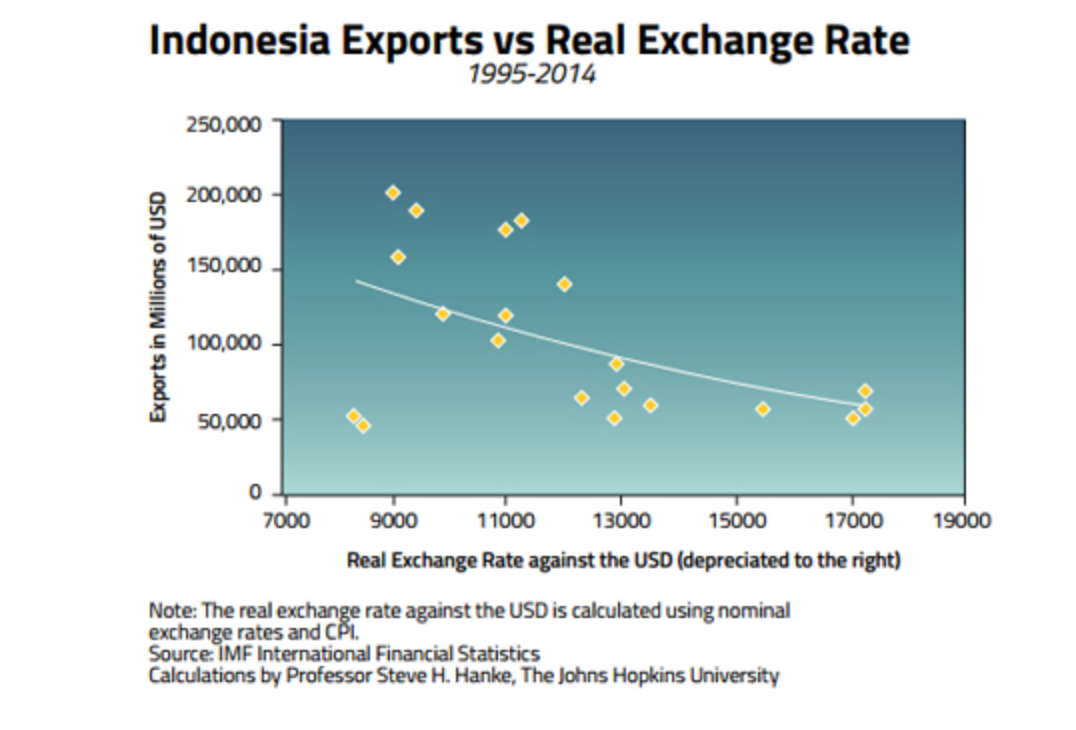

Other departures from theory have since occurred in recent decades. From 1995-2014, both China and Indonesia saw massive currency fluctuations against the US dollar, and contrary to expectations, exports increased when the currencies appreciated.[10]A devalued currency also correlates with slower GDP growth, illustrating that a weak currency is not always desirable. One link that has proven almost perfectly linear is the relationship between inflation and devalued currencies. “If we measure the strength of local currencies by the price of gold in those currencies, a virtual one-to-one relationship exists between the increase in the price of gold in a local currency (a weakening currency value) and a country’s annualized inflation rate”.[11]Another side effect of devaluation is an increase in local interest rates as investors demand a higher rate of return for investments denominated in a devalued currency.

Immunity from the issues of devaluation?

Governments have immense power when it comes to maintaining and regulating currency. They do this one of two ways, through either fiscal or monetary policy. Fiscal policy is a mechanism used to jolt or slow the economy by changing the amount of money the government spends and/or adjusting tax rates. Conversely, the central bank modulates monetary policy by changing the money supply, which changes interest rates to either stimulate or slow economic growth. But many people are now arguing that government shouldn’t have such unimpeded influence over setting the value of currency through these means. This suspicion has manifest itself in the form of cryptocurrencies, backed by a group of people who believe digital technology provides a future without government currency regulation.[12]Cryptocurrency supporters are skeptical of the Federal Reserve’s aims (monetary policy), and have attempted to neutralize the effects of inflation (that they believe plagues major currencies) by placing a finite cap on the amount of their coin. Unfortunately, it’s an uphill battle for cryptocurrency proponents. The volatility they claim to minimize has wreaked havoc on digital currencies in the year 2018 even more so than it has financial markets. Governments are retaliating by banning currencies such as Bitcoin and tightening their regulatory efforts against all cryptocurrencies. This makes sense as governments don’t want to relinquish control over their power to regulate currency. Governmental regulation almost always lags technological innovation, so further regulation is most likely on the horizon.

Egypt – a devaluation case study

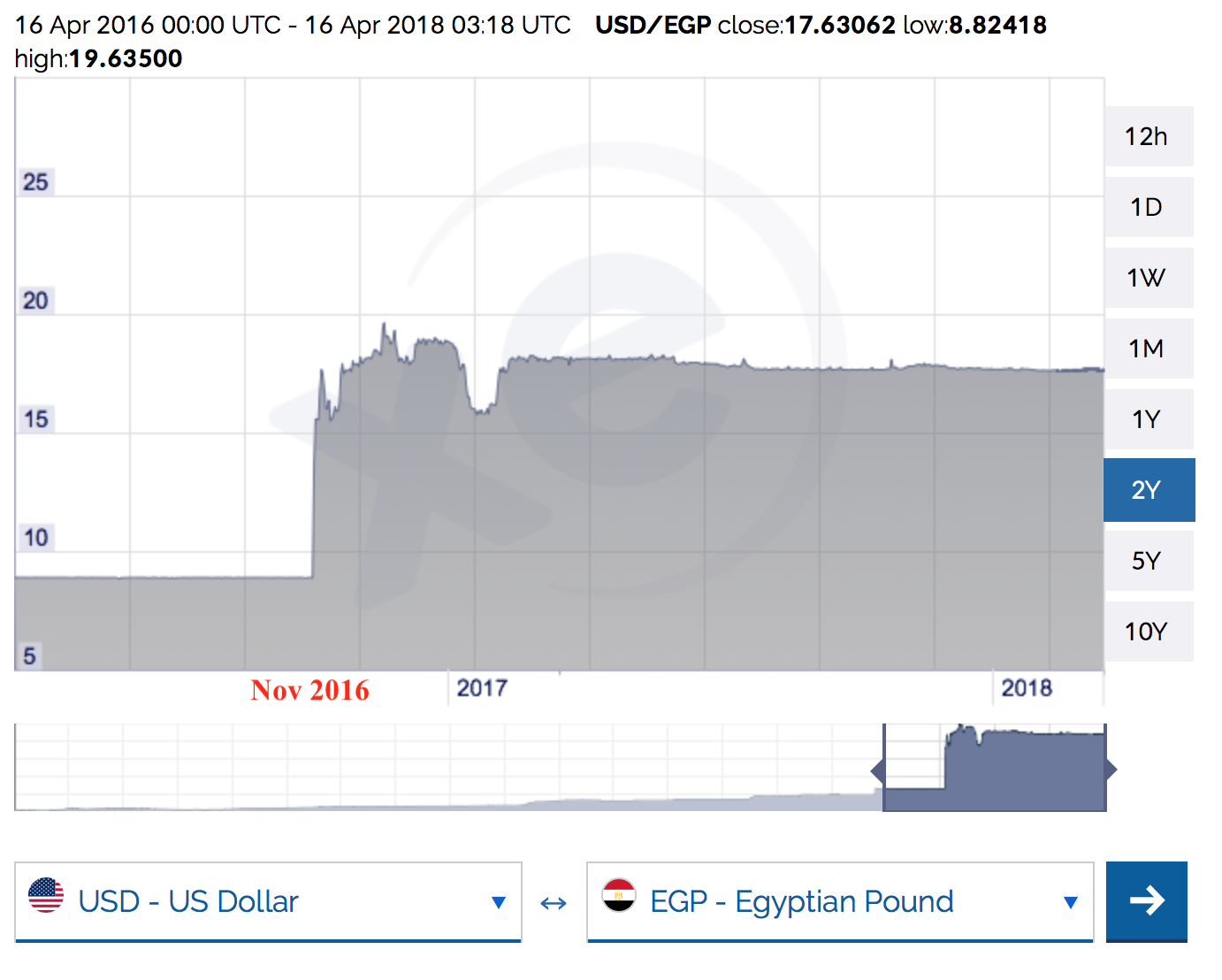

Egypt is one of the most recent and interesting cases of devaluation that merits close attention. In November of 2016, the Egyptian pound dropped 48% against the US dollar in a single day. The Egyptian economy had a severe shortage of foreign currency and they needed to stimulate foreign investment in order to reinvigorate the domestic economy. The devaluation was crucial in securing a $12 billion dollar bail out by the International Monetary Fund (IMF).[13]Following the mechanics of devaluation, Chris Jarvis, IMF Mission chief, stated devaluation would “improve Egypt’s external competitiveness, support exports and tourism and attract foreign investment. All of this will help foster growth, job creation and stronger external position for the country”.[14]As we’ve seen from a historical perspective, devaluation is inextricably linked with inflation. To reduce the impact inflation would have, the Egyptian central bank raised interest rates 3%. The higher interest rate makes the Egyptian Pound more attractive to foreign investors who can receive a higher rate of return, therefore stimulating foreign investment. But, Egypt is extremely dependent on both imports and tourism for the functioning of its economy. As previously addressed from a theoretical view, the price of imports skyrocket after inflation. Coupled with a drop in tourism, local businesses have struggled to keep doors open.

Prior to devaluation, the Egyptian Pound stood at 8.8 EGP per US dollar –as of April 2018, the rate is 17.62 EGP per US dollar. This should spur tourism and more foreign investment, especially when exchange rates stabilize and volatility drops.[15]Although the long term benefits for the Egyptian economy appear promising, local businesses have faced crippling inflation and increased borrowing costs resulting from higher interest rates. Businesses relying heavily on imports have seen their profits cut in half while inflation erodes general purchasing power (wage increases tend to lag behind inflation).[16]So although prices should double, businesses can only increase prices a fraction of that amount to keep pace with general purchasing power.

Conclusion:

Traditional debasement may not be present today but devaluation is much more common and is essentially an identical process. However, modern instances of devaluation illustrate an exposure to a variety of initially unforeseen variables. International political strife can lead to currency wars, while even a conscious effort to mitigate the negative effects of devaluation will leave the private sector scrambling in the short term. As we have seen, devaluation is considerably more complex than theories suggest. Furthermore, a distrust in the system has resulted in a group of cyberlibratarians who feel security by means of decentralized digitized currency outside government reach and supposedly immune to devaluation. Debasement is more prevalent now than it ever has been as we continue to see the pressures of globalization crunch certain currencies a disproportionate amount relative to others.

Written by Josh Chawla

References:

[1]John Locke, and P. H. Kelly. 1991. Locke on money. Oxford [England]; New York; Clarendon Press. Pg. 309.

[4]Lowndes, William.A Report Containing an Essay for the Amendment of the Silver Coins. England; United Kingdom; 1695. Pg. 3

[6]PYMNTS, “How Long Will Cash Stay On Top In The U.S.?” PYMNTS.com, August 10, 2017, accessed March 25, 2018, https://www.pymnts.com/cash/2017/united-states-cash-usage/.

[7]Brent Radcliffe, “Devaluation,” Investopedia, January 31, 2018, accessed March 25, 2018, https://www.investopedia.com/terms/d/devaluation.asp.

[8]Kimberly Amadeo, “2 Real Reasons for Inflation,” The Balance, August 12, 2017, , accessed March 25, 2018, https://www.thebalance.com/causes-of-inflation-3-real-reasons-for-rising-prices-3306094.

[9]Steve H. Hanke, “Currency Wars, the Devaluation Delusion,” Cato Institute, March 30, 2016, accessed March 25, 2018, https://www.cato.org/publications/commentary/currency-wars-devaluation-delusion.

[12]David Golumbia, The Politics of Bitcoin: Software as Right-wing Extremism (Minneapolis: University of Minnesota Press, 2016). Pg.8

[13]Zahraa Alkhalisi, “Egypt Devalues Its Currency by 48% to Clinch Bailout,” CNNMoney, November 03, 2016, accessed March 25, 2018, http://money.cnn.com/2016/11/03/news/economy/egypt-pound-devaluation-bailout/index.html.

[15]”The EGP Devaluation: A New Beginning,” PwC, accessed March 25, 2018, https://www.pwc.com/m1/en/publications/the-egp-devaluation-a-new-beginning.html.

[16]Heba Saleh, “Egypt Fights Inflation after Its Currency Devaluation,” Financial Times, December 12, 2017, accessed March 25, 2018, https://www.ft.com/content/dc2871fe-d4f9-11e7-8c9a-d9c0a5c8d5c9.