What is debasement?

Similar but different terms include depreciation and devaluation. Depreciation is a government-inflicted decrease in a currency relative to other currencies. Devaluation is the economy-influenced decrease in a currency relative to other currencies. Debasement is the physical reduction of a currency by weight or fineness (the percentage of precious metal in a coin) irrespective of relative value.

A brief overview of Debasement in England

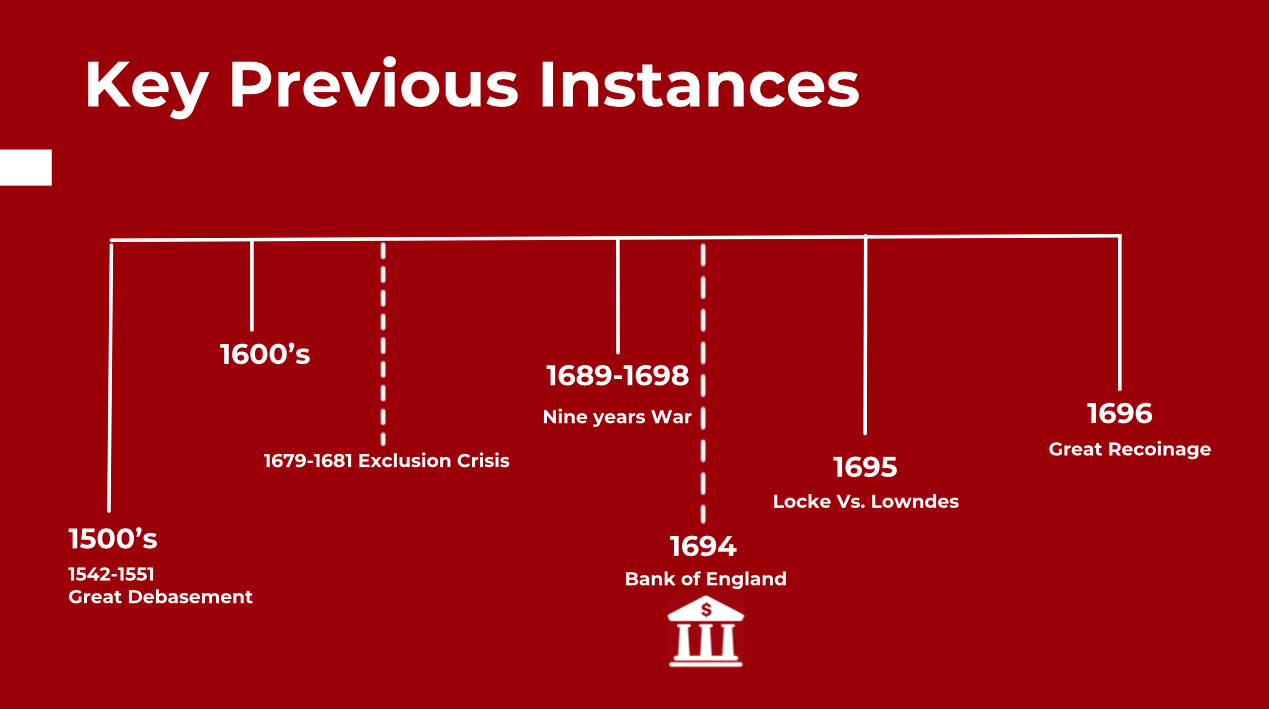

Debasement occurred throughout the 13-16oos in England. The following are some big-picture events. In the sixteenth century a couple kings wanted more money, so they debased the coin. Over a century later the Exclusion Crisis, in which many Brits split into Whigs and Tories with differing views on the (in)finite of wealth, occurred after a civil war. A few years later, England’s Revolution of 1688 brought them into conflict with France, and they entered into what has become known as the Nine Years War. Unfortunately for England, silver was valued more highly in some other European cities, so silver bullion was often exported. Additionally, much of the circulating coin was clipped or counterfeited. Therefore, there was not enough silver in England to pay for the war. The government’s solution was to create the Bank of England. However, the Bank was not able to raise enough funds, so the government resorted to recoinage. Recoining was intended to bring beat up coins back to the mint so that all coins could be standardized [1]. This became known as the Great Recoinage. Issues with debasement, nonetheless, continued until the Great Recoinage of 1816 when nominal value was at last favored over fineness [2].

Now to explain…

How?

Government officials in many countries have regularly reduced the metal content of money throughout history in order to maintain the monetary system. The three ways are to increase the face value of coin, decrease the size or weight of coin, or decrease the amount of valuable metal in coin [3]. In England, the dilution of coin continued over many regimes and across centuries [4].

The English tended to debase coin according to weight. Weight was a more favorable method to fineness because it is harder for an individual to detect a reduction in fineness than a reduction in weight since scales  could determine weight but there was not a tool available to laypeople to measure the proportions of the content. A brief experiment in the 14th century and Henry VIII’s Great Debasement were exceptions (See Theory and Mechanics) [5].

could determine weight but there was not a tool available to laypeople to measure the proportions of the content. A brief experiment in the 14th century and Henry VIII’s Great Debasement were exceptions (See Theory and Mechanics) [5].

Who controlled it?

The King in power and his government controlled the value of money. This is shown through the Great Debasement of the mid-16thcentury. Unlike earlier debasements that slightly diluted silver in order to re-stabilize the money supply, the Great Debasement, which compounded into a 74% lessening of silver content of coin, was a widely understood effort to raise revenues [6]. Henry VIII and, subsequently, his son Edward VI slowly decreased the silver and gold content of coin over ten years (1542-1551), normally announced, but when they desired larger gains they secretly debased as best they could [7]. The result of these debasements were an increase in coins, which were progressively less intrinsically valuable (contained less precious metal). Henry VIII and Edward VI nonetheless spent them as if they were the same in content [8]. Records show that the Great Debasement was even more effective in raising money for the government than taxation at the time [9].

Support?

Controversies did arise around money due to two distinct understandings of what money is. Some people were nominalists, meaning they believed that the value stamped on a coin indicated the coin’s worth. These people saw extrinsic worth in coin and supported debasement because it helped the economy without diminishing the value of money. This view, nominalism, supported debasement in England (see The Case of Mixed Money, 1605) [10]. The other understanding was one of identifying the value of coin intrinsically. A coin was intrinsically evaluated according to the amount of silver or gold in the coin, as measured by fineness and weight.

The Case of Mixed Money in Ireland was a court case in 1605 that was instigated by Queen Elizabeth’s directed creation of a new coin to be used in Ireland that was made with more base betal and less silver (mixed money) than the prior coin (sterling coin), which would continue in use in the rest of Britain [11]. The issue was that an Irish merchant (Brett) agreed to pay an English merchant (Gilbert) for some goods at a near future date. Before that day arrived, Queen Elizabeth ordered that the mixed money would replace the sterling coins as legal tender in Ireland. Therefore, when Brett met with Gilbert he brought 100 pounds of mixed money, which for Gilbert was worth less in London.  The dispute was whether Brett had paid enough to Gilbert or not. The council determined that Brett had paid Gilbert a legally sufficient sum. The conclusions were: it is necessary to have a standard of money in order to facilitate contracts, only the Crown of England can make or coin money, and the Crown may deem whatever he wants as money. This final conclusion includes the Crown’s ability to change the substance of money, enhance or debase the value, and even completely create or annul it [12].

The dispute was whether Brett had paid enough to Gilbert or not. The council determined that Brett had paid Gilbert a legally sufficient sum. The conclusions were: it is necessary to have a standard of money in order to facilitate contracts, only the Crown of England can make or coin money, and the Crown may deem whatever he wants as money. This final conclusion includes the Crown’s ability to change the substance of money, enhance or debase the value, and even completely create or annul it [12].

The debate in England over what money is and how its value is measured reached a critical point in the 1690s. A number of factors resulted in a nearly nonexistent intake of silver bullion at the mint after 1690 [13]. These factors included the consistent undervaluation of silver that influenced people to melt and export silver where it was deemed to have more worth, war decreased trade and the intake of bullion into England, what was imported had increasingly high price tags, the war required much of England’s money, and the coins that did exist were increasingly shrinking in size due to wear and tear and clipping [14]. In 1690, a House Committee recommended devaluing the silver coin, but even with a strong argument this plan was not immediately adopted. By 1695 silver coins weighed only half of their original weight when issued [15]. It was at this point that the Board at the Treasury was finally convinced to investigate the option of debasement.

The Board ordered the Secretary of the Treasury, William Lowndes, to create a case for devaluation. Lowndes produced “A report containing an essay for the amendment of the silver coins” later that year, in 1695. Some Whig politicians began to organize themselves in opposition to debasement in 1690, and among them was John Locke [16]. Locke responded to Lowndes’s report in the same year with this report: Further considerations concerning raising the value of money, wherein Mr. Lowndes’s arguments for it in his late report concerning An essay for the amendment of the silver coins, are particularly examined. Read about this debate in Debates and Contemporary Issues.

Conclusion

Overall, the English government utilized debasement when more money was desired or needed. Debasement was a consistent tactic throughout England’s history to influence the amount of money available.

Written by Nella Schools

References

[1] Christine Desan, Making Money: Coin, Currency, and the Coming of Capitalism. New York: Oxford University Press, 2014). 123.

[2] Kevin Clancy, “The recoinage and exchange of 1816-17.” (University of Leeds, 1999).

[3] Glen Davies, “The expansion of trade and finance, 1485-1640” in A History of Money: From Ancient Times to the Present Day. (University of Wales Press, 2010), 198.

[4] Desan, Making Money, 109.

[5] Desan, 121.

[6] Ibid. 232.

[7] Davies, “The expansion of trade and finance,” 199.

[8] Desan, 121.

[9] Davies, 202.

[10] Desan, 137.

[11] Ralph Benko, “The Case of the Mixed Money,” The Lehrman Institute, published July 19, 2012, http://www.thegoldstandardnow.org/key-blogs/1404-coinage-and-sovereignty.

[12] The Case of Mixed Money in Ireland. England. 1605.

[13] Desan, 341.

[14] Ibid. 342.

[15] Ibid.

[16] Ibid. 344.