Introduction

Monetary sovereignty is a foundational theory of economics that it is widely accepted and used across the globe in countries such as the United States and China. Simply put, monetary sovereignty is when a state has full legal control of its currency. This is rivaled by other forms of currency such as commodity money and monetary unions such as the countries in the Eurozone who decide to use the Euro, a currency controlled by the European Central Bank. As we will see in the theory section, monetary sovereignty offers many benefits to the nation states that adopt it, including more economic stability and reduced international influence of economic depressions abroad. This webpage will break down the theory and mechanics of monetary sovereignty, and highlight its pros and cons throughout.

Theory

Monetary sovereignty is a central theory necessary to understand the modern world’s money systems. This system is one where all of a nation’s currency is controlled by the state, and not by foreign countries or other forms of currency. “Monetary sovereignty in its contemporary sense signifies a sovereign right of a state to regulate all matters dealing with money issue and the conduct of monetary policy by a central bank with the purpose of achieving the projected economic policy targets.” (Salvatore and Dean, 141) A sovereign right is when a nation has full control over all aspects of itself, with no outside body having the ability to interfere. What does this mean for currency? It means what the state says goes, whether that be a change in the value of the currency or a change of the interest rates, the state has full legal control over their currency. Although many countries today utilize this system, it was developed long ago under monarchies in places like England. So what are the benefits of this system and why has it become such a dominant force? Chiefly, this theory was developed and gained significant traction as a “reaction against the international gold standard.”(Kurihara, 162) When a country adheres to a gold standard, their money’s value is directly tied to the value of gold. This undermines a country’s ability to be monetarily sovereign because the ability to control the value of their money is lost, as it fluctuates with the value of gold. This holds true for any commodity money: a money that is backed by a commodity like gold, silver, or crops.

In addition, being monetarily sovereign helps reduce the effect of economic depressions abroad from affecting one’s own state. For example, if a country under the Euro standard goes into recession, it will impact all member states’ economies negatively, whereas the United States (being monetarily sovereign) will be sheltered from the economic distress abroad. One other benefit is policy independence that a state has when there is a national bank controlling the currency. (Salvatore and Dean, 143) A central bank in a country has many abilities, “it can target the exchange rate, or the money supply or interest rates, and it can impose exchange controls or not.”(ibid) This runs in direct opposition to a collective monetary system such as the collection of countries who use the euro as their national currency, where an international debate about policy slows down and limits the ability to make policy changes such as the ones aforementioned. A second benefit is the ability to profit off of issuing currency. This is really only possible in a monetarily sovereign system as it is quite difficult to make arrangements to share this revenue across borders. The rate of inflation directly correlates to the amount of revenue a government makes of currency issuance, which can be controlled by a nation’s central bank but would be challenging to do internationally. As you can see, there are many benefits to being monetarily sovereign, demonstrating why it is such a dominant force throughout the world today.

Monetary sovereignty is unique and runs contrary to monetary unions such as the currency used by countries in the eurozone, the euro. Unlike countries like the United States with a national central bank, the euro is controlled by the European Central Bank, which is run by all of the countries in the eurozone. Although this is not a monetarily sovereign system, it is run quite similarly to national central banks such as the Federal Reserve. The next section of this paper describes the mechanics of the central banking system, which all applies to the European Central Bank as well. However similar in functioning, benefits such as sheltering a country from the harmful effects of depressions abroad does not apply because if any of the countries in the eurozone went into recession, it would affect all member states negatively as well.

Mechanics

Monetary sovereignty in today’s world is done through national central banking systems. For example, in the United States, currency is controlled by the Federal Reserve, which is the country’s central bank. Central banks play a huge role in their national economies, their responsibilities include: “issuing the national currency, acting as financial agents to governments, serving as a bankers’ bank, managing foreign exchange reserves and transactions, and conducting monetary and credit policies.”(Goodman, 6) These abilities of the central banking system are what make countries who utilize this type of system monetarily sovereign.

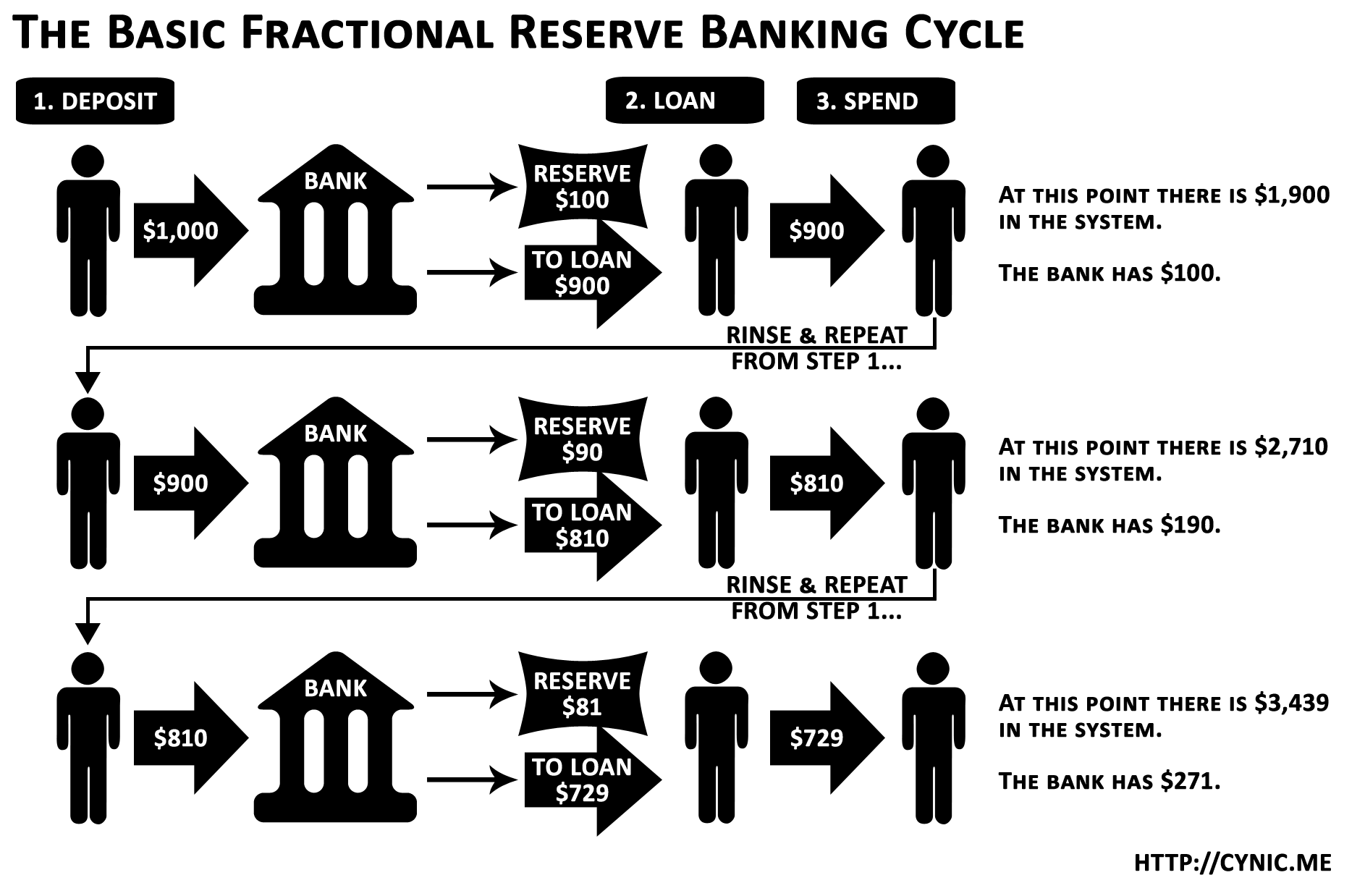

Debatably, the most important aspect of the central banking system is the control of a nation’s money supply. In modern times, most money that nations issue is intrinsically worthless and is considered fiat money. Fiat money is when a currency is backed just by a government’s word, with no tie to any commodity. So why does money carry value? First, the money has value because people are able to trust in the government’s ability to maintain that money’s value. Without this type of trust, fiat money would be impossible to accept as no one would trust that it would continue to hold its value. Secondly, the money gets its value “from its scarcity in relation to its usefulness.”(Federal Reserve Bank of Chicago, 3) Money’s value is contingent on its usefulness, or its ability to buy goods and services in the market. This partly comes from the trust in government that the money has value and the public’s acceptance of currency as a holder of value. Scarcity, or the quantity of money, is one of the central banks most important roles in the economy. The central bank cannot increase the money supply too much, because that would cause a harmful inflation in the economy. However, at the same time, they must make enough money to facilitate growth within the economy. Otherwise, unemployment would rise, and prices would fall, creating serious economic issues within the country. How does money get created? The quantity of money can be changed by these 3 actors: “Federal Reserve System (the central bank), depository institutions (principally commercial banks), or the public.”(ibid) This is true because of the fractional reserve banking system. Banks are able to issue notes of value as loans and investments as long as they have a certain amount of deposits that cover holders demand for actual currency.

Using this principle, the central bank is able to partially control the money supply through the sale government securities. This can change the amount of money in banks reserves, thereby controlling the creation of money by limiting the reserves of private banks. Fewer reserves mean less creation of money through the fractional reserve banking system. In addition to the selling of government securities, there is another tool that the Federal Reserve has to control the supply of money. The central bank can change the fractional reserve requirement of banks. This allows private banks to create more or less money depending on the percentage that they have to keep in their reserves relative to their loans and investments. Thus, by using both the sale of government securities and changing the fractional reserve requirement of banks, the Federal Reserve is able to control the money supply to keep the rate of growth of the value of money steady, preventing hyperinflation or deflation. This control of the money supply by the Federal Reserve is what makes the United States monetarily sovereign because the government has full legal control over the nation’s currency.

Without the central bank, governments would have to rely on other forms of money systems, whether that be commodity backed money, or private banking notes. However, without proper economic controls, the propensity for that money to be stable and consistent with growing economies would be slim. The central bank’s ability to regulate the supply of money, and the government’s ability to ensure trust in the value of that money, allows this type of money to function very successfully. That is why today there are less than 10 countries around the world who don’t use this type of banking system to manage their currency.

Utilizing this central banking model, countries around the world remain monetarily sovereign, exercising full legal control over their respective currencies. This has shown to be highly beneficial, especially in times of financial turmoil. Through the power of manipulating interest rates in conjunction with other monetary policies, the Federal Reserve was able to pull the United States out of the 2008 recession and restore the American economy. Utilizing these great tools, countries that remain monetarily sovereign through the central banking model are able to exercise full control over their money, creating a more stable and internationally independent economy and currency.

Now that you understand the theories and mechanics of monetary sovereignty, make sure to check out the other pages of our website! You can learn about other historical versions monetary sovereignty, as well as contemporary issues and debates about it. Thanks for reading.

Bibliography

Kurihara, Kenneth K. “Toward A New Theory of Monetary Sovereignty.” Journal of Political Economy 57, no. 2 (1949): 162-70. http://www.jstor.org/stable/1825189.

Nigel M. Healey, and Paul Levine. “European Monetary Union: The Issues.” Economic and Political Weekly 27, no. 6 (1992): 261-64. http://www.jstor.org/stable/4397558.

Zimmerman, Claus D. “The Concept of Monetary Sovereignty Revisited.” The European Journal of International Law24, no. 3 (2013).

Salvatore, Dominick, and James W. Dean. The Dollarization Debate. Oxford: Oxford University Press, 2003.

Goodman, John B. Monetary Sovereignty: The Politics of Central Banking in Western Europe. Ithaca, NY: Cornell University Press, 1992.

Federal Reserve Bank of Chicago. Modern Money Mechanics: A Workbook on Bank Reserves and Deposit Expansion. By Dorothy Nichols and Anne Marie Laporte. Gonczy. Chicago, IL: Federal Reserve Bank of Chicago, 1992.